Solar Panel Cost and Payback: The Assumptions Homeowners Need Before Comparing Quotes

I may earn a commission for purchases made through my links. It helps me run this site. Check out my disclosure for more details.

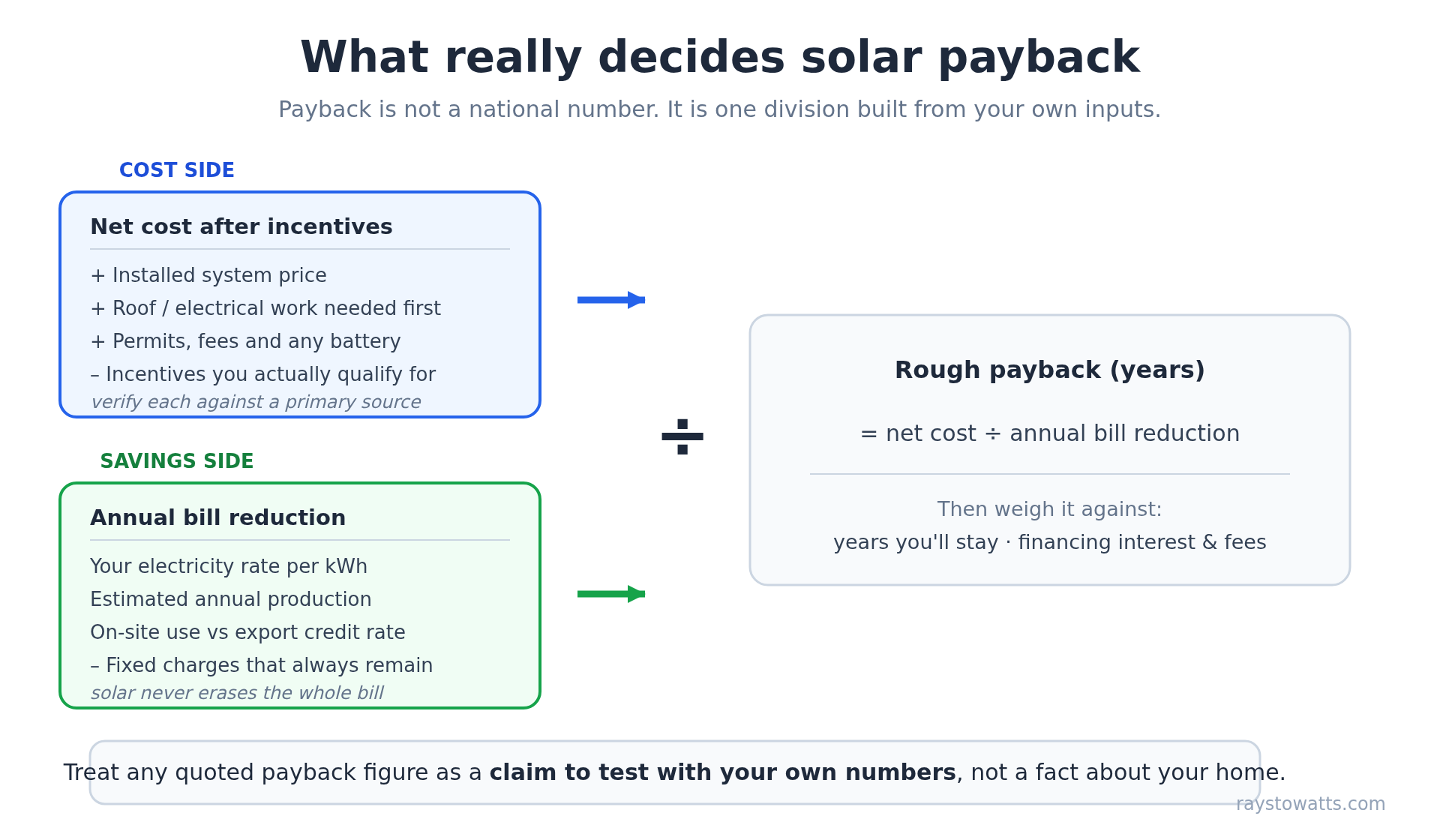

Solar payback is not a single national number. It is the result of your installed price, your electricity rate, the incentives you actually qualify for, how much your system produces, how you pay for it, and how long you keep the home. The useful skill is not memorizing an average payback year, it is learning the calculation so you can test any quote against your own numbers.

A payback period is the time it takes for the money a solar system saves (or earns through bill credits) to equal what you paid for it. That sounds simple, and that is exactly the problem. Every input in that calculation varies by home, utility, and contract. A figure that looks authoritative in a headline can be wrong for your roof by years. This page walks through each input, gives you a blank worksheet to fill with your own quotes, and flags where a number in a sales pitch deserves a second look.

This is general education, not financial advice. For decisions about your taxes or a specific contract, talk to a qualified tax professional or financial advisor.

Why payback is an assumptions problem

Two homes on the same street can have very different payback periods. One faces south with no shade, the other is shaded by an oak until noon. One owner pays a high electricity rate with favorable net metering, the other pays less and exports power for a smaller credit. One pays cash, the other finances at an interest rate that adds thousands over the loan term. Same panels, very different math.

Because of that spread, treat any single published payback figure as a starting hypothesis, not a fact about your home. The honest answer to “what is the payback on solar” is “it depends, and here is how to work out yours.” The federal government frames home solar the same way. The Department of Energy’s planning guide notes that online mapping tools “are an excellent starting point and can help you determine whether your home is suitable for solar,” but adds that “while these tools are helpful, they don’t account for all of the variables that need to be considered for your particular system.” The same caution applies to payback estimates.

The cost inputs: what you are actually paying for

The “cost” side of payback is more than the panel price. Build your number from these parts, using line items from real quotes rather than estimates:

- System size and installed price. Cost scales with system size, but not in a perfectly straight line. The Federal Trade Commission’s consumer guide states plainly that when you buy a system “you pay the entire cost of the system when it’s installed,” and “the cost depends on the size of the system.” Get the total installed price in writing.

- Equipment. Panels, inverters, mounting hardware, and any monitoring equipment. Higher-efficiency or premium equipment costs more upfront and may change the production assumption.

- Roof work. If your roof is near the end of its life, replacing it before installation is a real cost of going solar for you, even though it is not a “solar” line item. The DOE guide advises that “if you expect to need a new roof within the next few years, you may want to consider making that improvement before installing solar.”

- Permits and fees. The FTC notes that a complete bid should include “the full cost of installation, including any building or electrical permit fees.” Make sure these are in the quote, not added later.

- Batteries. Adding storage raises the upfront cost. Decide whether your goal is backup, bill management, or both before you treat a battery as part of the payback math, because a battery bought mainly for outage resilience is not primarily a savings device.

Record every one of these as a field you fill from quotes, not a figure you assume.

The savings inputs: where the credits come from

The “savings” side is where most optimistic estimates go wrong, because it depends on rules you do not control.

- Your utility rate. The more you pay per kilowatt-hour today, the more each kilowatt-hour of solar production is worth. Pull your last twelve months of bills. The FTC suggests you “add up the amount of ‘metered’ electricity or kilowatt-hours (kWh) of energy you used in the last year.”

- Fixed charges stay. Solar reduces the energy you buy, not the utility’s fixed fees. The FTC is direct about this: “When you use solar power, you don’t pay for as many kilowatt-hours, but you’ll still pay the utility’s fixed charges.” A payback estimate that assumes your whole bill disappears is wrong.

- Production. How many kilowatt-hours your system actually makes depends on system size, sun, shade, roof pitch, and direction. The FTC lists the factors that drive output, including “the average number of hours of direct, unshaded sunlight your roof gets annually” and “the pitch (angle), age, and condition of your roof, and the direction it faces.”

- Self-consumption versus export. Power you use as it is produced offsets electricity at your full retail rate. Power you export may be credited at a different, often lower, rate depending on your utility.

- Net metering and rate changes. Whether and how you are credited for exported power is set by your state and utility, and those rules change. The FTC advises homeowners to “contact your utility to see what arrangements it makes with homeowners who produce solar power,” noting that a utility “may use ‘net metering,’ which gives you credit for excess power your system makes and returns to the grid.” See our net metering explainer for how to verify your local rules.

Incentives and tax-credit treatment

Incentives lower your net cost, which shortens payback, but only the ones you actually qualify for count. Do not put an incentive into your math until you have confirmed it against a primary source.

The largest federal incentive has historically been the Residential Clean Energy Credit. This credit is date-sensitive, and the rules have a near-term cutoff, so verify the current status on the IRS page before you rely on it. As of this article’s review date, the IRS states: “The Residential Clean Energy Credit equals 30% of the costs of new, qualified clean energy property for your home installed anytime from 2022 through December 31, 2025. The credit is not available for any property placed in service after December 31, 2025.”

A few details that change how the credit affects your payback math:

- It is nonrefundable. The IRS states the credit “is nonrefundable, so the credit amount you receive can’t exceed the amount you owe in tax,” though you “can carry forward any excess unused credit.” A credit only helps your payback to the extent you have tax liability to apply it against.

- Rebates and subsidies can reduce the basis. The IRS notes that “public utility subsidies for buying or installing clean energy property are subtracted from qualified expenses,” while “utility payments for clean energy you sell back to the grid, such as net metering credits, don’t affect your qualified expenses.”

- Loan interest does not count. The IRS says to “not include interest paid including loan origination fees” in the credited cost.

State, utility, and local incentives can also apply, but these go stale quickly and vary by location. Verify each one against the program administrator before counting it, and see our guide on checking state and utility incentives. Do not rely on an installer’s sales sheet or an affiliate page as your authority for any tax or incentive claim.

Financing changes the math

How you pay for the system changes both the cost and the rights attached to it. The FTC frames the core choice this way: “If you want to use solar power for your home, your options include buying a system, leasing a system, or signing an agreement to buy solar power.”

- Cash. You pay the full installed price upfront and keep all the savings and any incentives you qualify for. Payback is the cleanest to calculate.

- Loan. You spread the cost, but interest and fees add to the total you pay, which lengthens payback. Remember the IRS treatment above: loan interest is not part of the credited cost.

- Lease or PPA. You may pay little or nothing upfront, but you typically do not own the system, which affects who claims incentives and how a sale of the home works. The FTC warns that depending on your option “you might get certain tax breaks or need to take extra steps before selling your home.”

Our financing options guide compares cash, loan, lease, and PPA in more detail. The key point for payback: only a model where you own the system lets you count the federal credit toward your own cost, and only if you have the tax liability to use it.

Payback worksheet

Fill these fields from your own bills and written quotes. Leave them blank until you have a real number. Do not substitute a national average for any field.

Cost side

- Installed system price (from quote): __________

- Roof or electrical work needed first: __________

- Battery (if any): __________

- Permits and fees (confirm included): __________

- Total upfront cost: __________

- Federal credit you qualify for (verify on IRS page): __________

- State, utility, or local incentives (each verified): __________

- Net cost after incentives: __________

Savings side

- Your current electricity rate (per kWh, from bill): __________

- Annual kWh you use (last 12 months): __________

- Estimated annual production (from installer model): __________

- Share used on-site versus exported: __________

- Export credit rate (from utility): __________

- Utility fixed charges that remain: __________

- Estimated annual bill reduction: __________

Result

- Net cost divided by annual bill reduction = rough payback in years: __________

- Years you plan to stay in the home: __________

- Financing interest and fees (if any), added to cost: __________

Worked example (illustration only, not a claim about your home)

This example uses round, clearly labeled assumptions to show how the worksheet flows. None of these numbers are a national average or a claim about real costs. Replace every figure with your own.

Assume an installed cost of $X after a verified incentive total of $Y, for a net cost of $Z. Assume the system reduces your annual electricity spending by $A, calculated from your real rate and a production estimate from the installer. Then the rough payback is $Z divided by $A, in years, before financing costs. If you financed the system, add the interest and fees to the cost side first. If you plan to move before that payback year arrives, the system may not pay for itself through bill savings alone, which is when resale value and contract transfer terms matter.

The point of the example is the structure, not the digits. A quote is credible when its payback claim survives this worksheet with your real inputs.

When a payback claim in a quote needs a second look

Treat a quoted payback figure as a claim to test, not a promise. Look closer when a quote:

- Assumes your whole bill disappears. Fixed charges remain, as the FTC notes. A payback built on a zero bill is too optimistic.

- Uses a production estimate you cannot trace. Ask which tool or model produced the kilowatt-hour figure and what shade and orientation assumptions it used.

- Counts incentives you have not verified. A credit you do not qualify for, or one past its cutoff date, does not shorten your real payback.

- Builds in steep utility rate increases. Assuming large annual rate hikes makes any payback look faster. Ask what rate growth the estimate assumes.

- Ignores financing cost. A low monthly payment can hide a long total payback once interest is included.

A battery runtime calculator (coming soon) will help you size backup loads separately from this payback math, since a battery bought for resilience is not primarily a savings tool.

FAQ

Does adding a battery change my payback? Usually it lengthens it, because a battery adds upfront cost and its main value is often backup power rather than bill savings. Decide whether your goal is outage resilience, bill management, or both before you fold a battery into payback math. Battery storage may qualify for the federal credit; the IRS lists “battery storage technology (beginning in 2023)” among qualified expenses, but confirm the current rules and cutoff date on the IRS page.

How does my ownership horizon affect payback? If you plan to move before the system pays for itself through bill savings, payback through savings alone may not complete. The FTC notes a residential system “is designed to stay on a home for at least 20 years,” and advises that if you might move you should “find out how buying and installing a system, compared to leasing a system or signing a PPA, might affect your ability to sell your house.”

I have a very high electricity bill. Is payback automatic? A high bill and high rate generally make each kilowatt-hour of solar more valuable, which can shorten payback, but it is not automatic. Production, shade, net-metering rules, and financing still decide the result. Run the worksheet with your real numbers.

I have a low bill. Is solar still worth considering? With a low bill the savings per year are smaller, so payback tends to be longer. That does not rule solar out, but it raises the bar for the cost and financing terms that make sense. Our “is solar worth it” checklist walks through this.

My roof is shaded. How does that affect the math? Shade reduces production, which reduces annual savings and lengthens payback. The FTC lists unshaded sunlight hours and roof orientation among the factors that determine output. A credible quote should account for your actual shade, not assume an unshaded roof.

Why not just trust a national average payback? Because the inputs that decide payback (your rate, incentives, production, financing, and ownership horizon) all vary by home. A national average can be off by years for your situation. Use it for context only, and base decisions on your own worksheet.

—

*Affiliate disclosure: some links on RaysToWatts may earn us a commission at no extra cost to you. We only suggest comparing quotes after you have run your own numbers.*

*Ready to test real numbers against this worksheet? Comparing multiple detailed quotes is the way to see whether a payback claim holds up for your home. The FTC recommends you “compare detailed bids from several companies.” When you are ready, you can compare solar quotes from vetted marketplaces.*

*This article is general information, not financial or tax advice. Incentive and tax rules change; confirm current details with primary sources and a qualified professional before relying on them.*